Bankers Petroleum in Albania: Production Halt, Tax Dispute, and Rising Labour Anger Converge

Bankers Petroleum Albania—operator of the Patos-Marinzë oilfield—has been hit by a fast-moving convergence of crises that now threatens both output and stability in one of Albania’s most strategic industrial zones. Within the space of roughly 24 hours, the company’s production activity was effectively frozen by customs authorities, while workers and subcontractors intensified protests over pay and working conditions, raising fears of a wider operational breakdown and renewed political escalation.

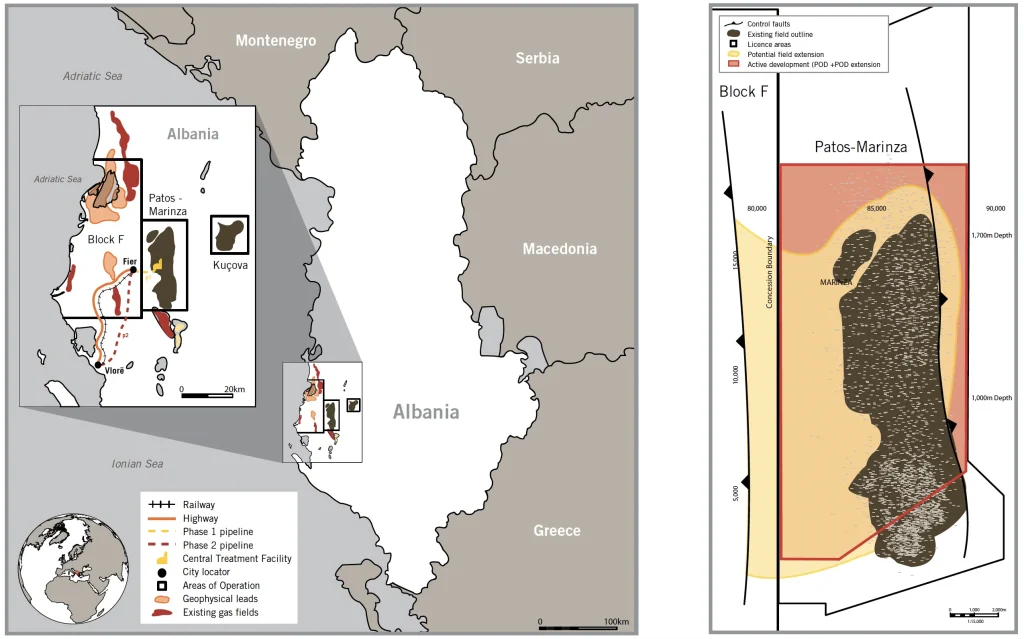

Customs blockade stops extraction at Patos-Marinzë

The most immediate shock came from the General Directorate of Customs, which—according to multiple Albanian media reports citing the company—ordered the blocking of Bankers Petroleum’s production and financial activity at the Patos-Marinzë extraction facilities. The stated trigger is an excise-tax dispute tied to the “diluent” used in heavy-oil production: customs authorities argue the company has not paid excise obligations for this input.

Bankers Petroleum’s response frames the action as arbitrary and procedurally unlawful, arguing that the diluent should not be subject to excise because it is not consumed in Albania and is used as a technical input in extracting and transporting crude that is exported. The company also points to a long-running legal conflict over this same issue, describing it as a matter still in court rather than one that should be enforced via an immediate operational shutdown.

Report TV links the current enforcement move to a much larger historical penalty: a fine totaling €120 million, reportedly assessed in 2019 after a customs investigation concluded Bankers had avoided at least €30 million in excise obligations related to diluent, with a further €90 million calculated as a penalty.

A technical shutdown with high-stakes consequences

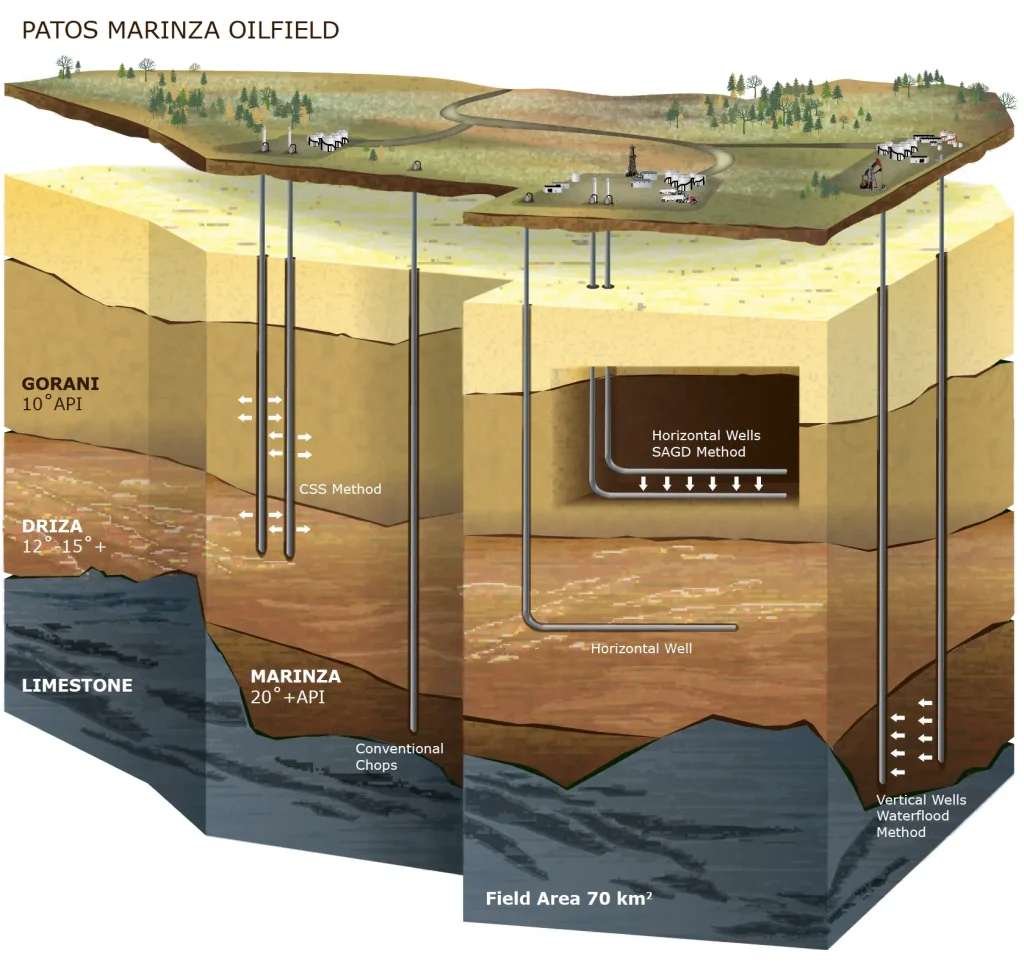

Beyond the legal argument, Bankers and sector officials warn the stoppage is not a simple “pause.” Heavy crude at Patos-Marinzë requires continuous handling; once cooling begins, viscosity rises sharply and oil can solidify inside pipelines and storage infrastructure. In the company’s account—also quoted by Gazeta Shqip—Albania’s National Agency of Natural Resources (AKBN) has warned that extraction must run continuously (24/7) to avoid the crude becoming unusable in pipelines and tanks, and that storage constraints can force a full field shutdown with wider safety and environmental risks.

This is a critical point because it redefines the customs decision from a financial enforcement measure into an operational hazard: if the field is shut in abruptly, restarting can be technically difficult, expensive, and in some wells impossible—an argument Bankers uses to portray the blockade as disproportionately damaging to the Albanian state as resource owner, not only to the operator.

Labour unrest: “unpaid November” and a protest that is no longer isolated

While the customs dispute escalated at the institutional level, the social front has also heated up. The protest on 16 December 2025 did not appear in a vacuum. Earlier reporting through 2025 describes repeated mobilisations—demands for wage increases, implementation of collective agreements, improved working conditions, and recognition of oil-worker status. In October, workers were also reported to have entered a hunger strike, urging the state to mediate more actively. Bankers, for its part, previously acknowledged industrial action and union pressure but insisted production had continued normally during the strike period and pointed to planned increases in allowances while rejecting further wage hikes due to “financial pressures,” including oil-price weakness and exchange-rate effects. The risk is that each pressure point amplifies the other: when workers fear wages are at risk, a state-ordered shutdown looks like confirmation; when the state sees instability, enforcement can harden.

A broader legal cloud hangs over the operator

Layered onto the operational and labour crisis is an expanding legal narrative around Bankers Petroleum’s finances.

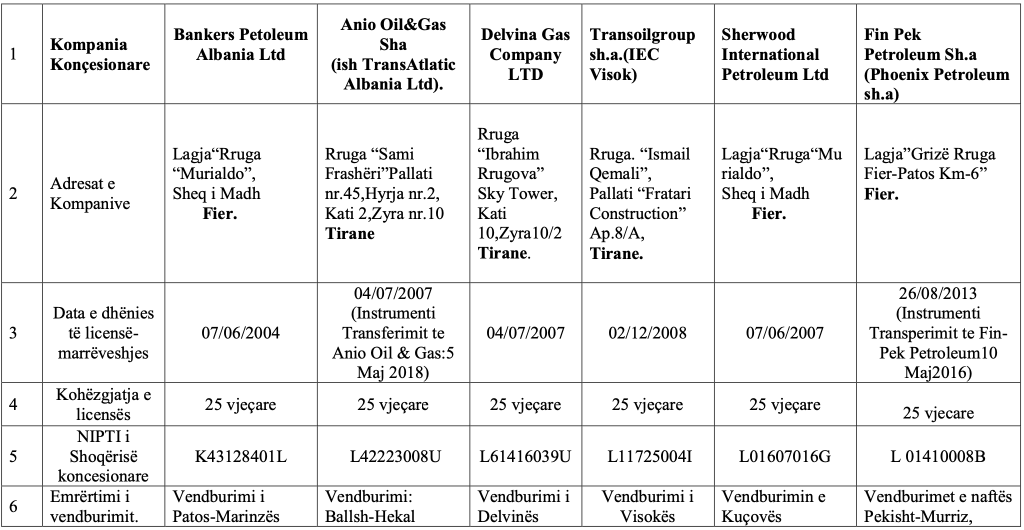

Albania’s Prosecutor’s Office in Fier described an investigation alleging Bankers Petroleum Albania Ltd engaged in fraudulent schemes related to VAT, concealment of income, money laundering, and other offenses, with precautionary measures taken against multiple individuals and others declared wanted. The same source release claims the company reported losses consistently from 2004 through 2024, despite large volumes of exports and domestic sales, and alleges damages to the state budget linked particularly to fraudulent VAT claims.

This backdrop matters because it shapes how every new development is interpreted. For critics, the customs blockade and wage protests reinforce a narrative of a politically protected operator now facing overdue accountability. For the company, aggressive enforcement is portrayed as premature, legally questionable, and capable of destroying assets that ultimately belong to the Albanian public.

What is happening now—and what happens next

As of 16 December 2025, the situation around Bankers Petroleum can be summarised as a three-front confrontation:

-

Institutional enforcement: Customs has moved to block operations over a contested excise obligation tied to diluent, with references in reporting to a much larger unresolved fine dating back to 2019.

-

Operational risk: AKBN warnings cited in media coverage underline that halting heavy-oil production can cause technical damage and safety risks if the system is not managed carefully.

-

Workforce instability: Protests and claims of unpaid wages—especially among subcontractors—indicate growing social stress at the field level, with political actors amplifying the message and demanding state intervention.

The immediate next steps are likely to unfold across institutions rather than at the wellhead: pressure on the Ministry of Finance to intervene, continued court and prosecutorial actions, and negotiations (formal or informal) over how the field can be kept safe and technically stable while legal disputes continue. The deeper question—still unresolved—is whether Albania’s largest onshore oil operation can sustain output and social peace while sitting at the intersection of labour conflict, tax enforcement, and criminal investigation.

If the blockade persists, the costs will not be measured only in barrels lost, but also in jobs, contractor liquidity, community safety, and the credibility of the state’s ability to regulate strategically vital assets without triggering destabilising shocks.

Bankers Petroleum Albania — operatori i fushës naftëmbajtëse Patos-Marinzë — është goditur nga një përqendrim krizash me zhvillim të shpejtë, që tashmë kërcënon si prodhimin ashtu edhe stabilitetin në një nga zonat industriale më strategjike të Shqipërisë. Brenda rreth 24 orëve, aktiviteti prodhues i kompanisë u ngrirë praktikisht nga autoritetet doganore, ndërsa punëtorët dhe nënkontraktorët intensifikuan protestat për pagat dhe kushtet e punës, duke rritur frikën për një prishje më të gjerë të operacioneve dhe një përshkallëzim të ri politik.

Bllokada doganore ndal nxjerrjen në Patos-Marinzë

Goditja më e menjëhershme erdhi nga Drejtoria e Përgjithshme e Doganave, e cila — sipas disa raportimeve të mediave shqiptare që citojnë kompaninë — urdhëroi bllokimin e aktivitetit prodhues dhe financiar të Bankers Petroleum në impiantet e nxjerrjes në Patos-Marinzë. Shkaku i deklaruar lidhet me një mosmarrëveshje për akcizën, që ka të bëjë me “diluentin” e përdorur në prodhimin e naftës së rëndë: autoritetet doganore argumentojnë se kompania nuk ka paguar detyrimet e akcizës për këtë input.

Reagimi i Bankers Petroleum e paraqet veprimin si arbitrar dhe procedurialisht të paligjshëm, duke argumentuar se diluenti nuk duhet t’i nënshtrohet akcizës, sepse nuk konsumohet në Shqipëri dhe përdoret si input teknik në nxjerrjen dhe transportin e naftës së papërpunuar që eksportohet. Kompania thekson gjithashtu se ekziston një konflikt ligjor i kahershëm për të njëjtën çështje, duke e përshkruar si një materie ende në gjykatë dhe jo diçka që duhet zbatuar përmes një mbylljeje të menjëhershme të operacioneve.

Report TV e lidh këtë lëvizje aktuale të zbatimit me një penalitet historik shumë më të madh: një gjobë totale prej 120 milionë eurosh, e cila thuhet se është vendosur në vitin 2019, pasi një hetim doganor konkludoi se Bankers kishte shmangur të paktën 30 milionë euro detyrime akcize që lidhen me diluentin, ndërsa 90 milionë euro të tjera u llogaritën si penalitet.

Një ndalim teknik me pasoja të mëdha

Përtej argumentit ligjor, Bankers dhe zyrtarë të sektorit paralajmërojnë se ndalimi nuk është një “pauzë” e thjeshtë. Nafta e rëndë në Patos-Marinzë kërkon trajtim të vazhdueshëm; sapo fillon ftohja, viskoziteti rritet ndjeshëm dhe nafta mund të ngurtësohet brenda tubacioneve dhe infrastrukturës së depozitimit. Sipas përshkrimit të kompanisë — i cituar edhe nga Gazeta Shqip — Agjencia Kombëtare e Burimeve Natyrore (AKBN) ka paralajmëruar se nxjerrja duhet të funksionojë pandërprerë (24/7) për të shmangur bërjen të papërdorshme të naftës në tubacione dhe depozita, si dhe se kufizimet e magazinimit mund të detyrojnë mbyllje të plotë të fushës, me rreziqe më të gjera për sigurinë dhe mjedisin.

Ky është një element kritik, sepse e riformulon vendimin e doganave nga një masë zbatimi financiar në një rrezik operacional: nëse fusha mbyllet papritur, rifillimi mund të jetë teknikisht i vështirë, i kushtueshëm dhe në disa puse i pamundur — një argument që Bankers e përdor për ta paraqitur bllokadën si proporcionalisht dëmtuese edhe për shtetin shqiptar si pronar i burimit, jo vetëm për operatorin.

Pakënaqësia e punës: “nëntor i papaguar” dhe një protestë që s’është më e izoluar

Ndërsa mosmarrëveshja me doganat u përshkallëzua në nivel institucional, edhe fronti social është tensionuar. Protesta e 16 dhjetorit 2025 nuk u shfaq në boshllëk. Raportime më të hershme gjatë vitit 2025 përshkruajnë mobilizime të përsëritura — kërkesa për rritje pagash, zbatim të marrëveshjeve kolektive, përmirësim të kushteve të punës dhe njohje të statusit të punëtorit të naftës. Në tetor, punëtorët raportohet se hynë edhe në grevë urie, duke i kërkuar shtetit të ndërmjetësonte më aktivisht. Bankers, nga ana e vet, më parë e pranoi ekzistencën e veprimeve industriale dhe presionin sindikal, por këmbënguli se prodhimi kishte vijuar normalisht gjatë periudhës së grevave dhe përmendi rritje të planifikuara të dietave/kompensimeve, ndërsa hodhi poshtë rritje të mëtejshme pagash për shkak të “presioneve financiare”, përfshirë dobësinë e çmimeve të naftës dhe efektet e kursit të këmbimit. Rreziku është që secili presion ta amplifikojë tjetrin: kur punëtorët druhen se pagat janë në rrezik, një mbyllje e urdhëruar nga shteti shihet si konfirmim; kur shteti sheh paqëndrueshmëri, zbatimi i masave mund të ashpërsohet.

Një re më e gjerë ligjore mbi operatorin

Mbi krizën operative dhe të punës shtresohet edhe një narrativë ligjore në zgjerim rreth financave të Bankers Petroleum.

Prokuroria e Fierit përshkroi një hetim që pretendon se Bankers Petroleum Albania Ltd është për leaving në skema mashtruese të lidhura me TVSH-në, fshehje të të ardhurave, pastrim parash dhe vepra të tjera penale, me masa sigurie ndaj disa personave dhe të tjerë të shpallur në kërkim. E njëjta deklaratë pretendon se kompania ka raportuar humbje në mënyrë të vazhdueshme nga 2004 deri në 2024, pavarësisht volumeve të mëdha të eksportit dhe shitjeve brenda vendit, dhe ngre pretendime për dëme në buxhetin e shtetit, veçanërisht të lidhura me kërkesa të rreme për rimbursim/kompensim të TVSH-së.

Ky sfond ka rëndësi, sepse formëson mënyrën se si interpretohet çdo zhvillim i ri. Për kritikët, bllokada doganore dhe protestat për paga forcojnë një narrativë se një operator i mbrojtur politikisht po përballet më në fund me llogaridhënie të vonuar. Për kompaninë, zbatimi agresiv paraqitet si i parakohshëm, i diskutueshëm ligjërisht dhe i aftë të shkatërrojë asete që në fund i përkasin publikut shqiptar.

Çfarë po ndodh tani — dhe çfarë mund të ndodhë më pas

Që nga 16 dhjetori 2025, situata rreth Bankers Petroleum mund të përmblidhet si një përballje në tre fronte:

-

Zbatim institucional: Doganat kanë lëvizur për të bllokuar operacionet mbi një detyrim të kontestuar akcize të lidhur me diluentin, me referenca në raportime për një gjobë shumë më të madhe të pazgjidhur që daton nga viti 2019.

-

Rrezik operacional: Paralajmërimet e AKBN-së të cituara në mbulim mediatik nënvizojnë se ndërprerja e prodhimit të naftës së rëndë mund të shkaktojë dëme teknike dhe rreziqe sigurie nëse sistemi nuk menaxhohet me kujdes.

-

Paqëndrueshmëri e fuqisë punëtore: Protestat dhe pretendimet për paga të papaguara — veçanërisht nga nënkontraktorët — tregojnë rritje të stresit social në nivel fushe, me aktorë politikë që e amplifikojnë mesazhin dhe kërkojnë ndërhyrje të shtetit.

Hapat e menjëhershëm ka gjasa të zhvillohen më shumë nëpër institucione sesa te pusi: presion mbi Ministrinë e Financave për të ndërhyrë, vijim i proceseve gjyqësore dhe veprimeve prokuroriale, si dhe negociata (formale ose joformale) për mënyrën se si fusha mund të mbahet e sigurt dhe teknikisht e qëndrueshme ndërsa mosmarrëveshjet ligjore vazhdojnë. Pyetja më e thellë — ende e pazgjidhur — është nëse operacioni më i madh tokësor i naftës në Shqipëri mund të ruajë prodhimin dhe paqen sociale, teksa gjendet në kryqëzimin e konfliktit të punës, zbatimit tatimor dhe hetimit penal.

Nëse bllokada vazhdon, kostot nuk do të maten vetëm me fuçi të humbura, por edhe me vende pune, likuiditet të kontraktorëve, siguri komunitare dhe me besueshmërinë e aftësisë së shtetit për të rregulluar asete strategjikisht jetike pa shkaktuar tronditje destabilizuese.